Two-in-one: AMS:AALB & LON:WEIR

Getting exposure to the green agenda by way of two high-quality compounders

It has been a while since I last shared an investment idea - and for good reason. Transitioning from academia to the fast-paced world of investment banking has been quite the journey, but I've been hard at work curating a lineup of potential winners for you. In mid-January, I offered an exclusive deep dive into Aalberts (AMS:AALB) - as a special thank you to those of you who have pledged their monetary support for my research efforts. Aalberts’ recently published full-year results only serve to reinforce the insights shared in my analysis (PT: €60/share). For access to the report, feel free to reach out to me directly on Twitter/X at thepiccledotcom.

In addition to the Aalberts write-up, I'll delve into another company - The Weir Group (LON:WEIR) - in this post. Despite their inherent differences, both companies were chosen to offer quality exposure to the green transition - without compromising on my key investment criteria (listed in this post). Without further ado, lets dive right in!

0. Initiating position

On the back of The Weir Group's FY24 results announcement, shares slumped -8%, presenting a good entry point for me to get exposure to a secular trend I have long been following. I managed to get in at an average price of GBP 17.70/share, capitalizing on the negative earnings reaction as shares quickly rebounded +13%. Nonetheless, I believe there is further upside ahead. My conservative estimates suggest a target price of GBP ~25/share, indicating a +20% upside from the latest closing price and a robust +40% return on my initial investment. I anticipate this will materialize over the course of the coming 3-4 quarters, and thus I will pay meticulous attention to possible thesis drift to uphold investment returns (i.e. closing position early if data-points/leading indicators suggest so).

1. Introduction

Founded in 1871, The Weir Group is a market leading OEM of heavy equipment and associated aftermarket services (77% of FY23A sales) to the mining industry. Over the past decade, the company has transformed itself into a pure-play mining business - marked by the divestment of its P&I segment (2019) and O&G segment (2021). What is left is a less risky mid/downstream mining equipment company with financial visibility, high (and expanding) ROIC, a sticky customer base, and resiliency to grow through the cycle. In fact, Weir, excluding its P&I and O&G business, has grown at a CAGR of 6.1% with a standard deviation of 11.2% from 2008-22. Significantly higher organic growth rates at lower volatility versus its peers.

The company consists of two segments: 1) Weir Minerals (73% of FY23A sales) which provides heavy equipment and services for the Comminution (crushing & grinding of ores) and Beneficiation (process of improving the concentration of mined minerals) activities in the mining value chain. 2) Weir ESCO (27%) which was formed on the back of an acquisition in 2018 (EV $1,250m), and operates in a tight pocket of the market characterized by high levels of re-occurring aftermarket sales (94% of FY23A Weir ESCO sales). The segment provides surface mining products (i.e. ground-engaging tools), and thus is present in present in the Extraction process (upstream). Since the acquisition, the segment has been complemented by a few smaller add-ons (i.e., Motion Metrics (2021, EV £89m), and CIS (2022, EV £20m). Below is an overview of the value chain and the different players present in each step:

2. Thesis

My thesis rests on both systematic (industry-related) and idiosyncratic (company related) elements. Below I provide a break-down of why I am bullish on mining OEMs generally - and why I have believe Weir is the better company to be invested in.

Systematic: Bullish on mining OEMs

The structural supply-gap for critical minerals, such as copper, nickel, and lithium, is well documented. According to research from JPM, 2023 was the last year where copper supply and demand were in an equilibrium. That means from now and onwards, supply will not be sufficient to meet demand:

Although the abovementioned supply-gap has been known for long, miners have been hesitant to put new mines online, leaving them with an underinvested asset base. In fact the average equipment age is estimated to be >8 years with >28% originally purchased in 2010 or earlier. Instead, miners have sought to sweat their assets and dig deeper into the ground where ore grades are lower (I.e., c.1pp deterioration over the last 30 years in the case of copper). As such, miners have to feed more volumes into its equipment to yield the same output - wearing assets even harder. This drives demand for aftermarket services, both by way of upgrades/modifications to the existing base (I.e., improving efficiency) as well as consumables (I.e. spare/wear parts, lubes, etc.).

The above factors are not going away anytime soon as it takes 7-10 years to bring a new mine online. Also, several miners are challenged by permitting issues - further delaying the odds of new mines being put online in due time. In fact, some miners are explicit about not brining new supply online, best exemplified by this statement by Glencore’s CEO, Gary Nagle:

“We believe the [copper supply] deficit is real, but we will only see if it is real if the price is real. When the price is there, and the world is screaming for the copper that it needs, and we are a few dollars away from demand destruction that is the time that we will bring on this copper to meet that demand.”

Idiosyncratic: Picking Weir as the winner

As depicted in the mining equipment value chain, shown above, the number of listed players in the mid/downstream are limited (Metso Outotec, FLSmidth, and Weir). All players have unique - and sometimes attractive - elements to their equity story. I was (and still am) particularly intrigued by the potential upside embedded in FLSmidth which benefits from a successful self-help story, favorable commodity mix, and “straightforward” near-term margin expansion:

Self-help: The company is making tangible progress (and faster than anticipated) with regards to its shift toward becoming a pure-play mining player; fully exiting the cement industry and winding down of non-core activities/bad projects by end of 2024.

Favorable exposure: It is the company with the highest exposure to critical minerals, with sales to copper miners making up ~40% (vs. c.25% for Weir).

Near-term margin expansion: TK Mining acquisition instantly added a large installed base (takes years on end to build a meaningful installed base) with huge unpenetrated aftermarket opportunity (TKM had only c.30% AM sales). This, coupled with cost synergies far exceeding what was initially expected (DKKm 600 vs. DKKm 360) should bode well for the company in the near term.

However, what sets Weir apart from all of its peers is the unmatched - and high quality - aftermarket exposure. Aftermarket sales consistently account for 75-80% of Weir’s sales (vs. 60-65% for FLSmidth and Metso Outotec). Not only that, but the quality of said aftermarket sales is better than that of both peers’.

c.30-35% of Metso and FLS aftermarket sales are from modifications and upgrades (i.e. professional services that are likely to be impacted first during a downturn as miners curtail discretionary spend). This figure is closer to 20% for Weir. As such, a higher share of Weir aftermarket sales are non-discretionary, shielding the company from macroeconomic turbulence.

In addition to the above, Weir is leading within technologies/products where annual spend on spares are high (I.e. pumps & cyclones):

Sure, peers are also committed to expand their aftermarket presence which may put pressure on Weir’s market share. To be frank, this is not something I am too worried about in the medium term. For one, it has been a “theme” to grow aftermarket sales since before GFC for most mining OEMs, and while they have indeed expanded the pace has been much slower than anticipated. Second, stickiness is real. Most miners tend to stay with the OEM in the aftermarket domain - both because this is needed if they want to stay covered by warranties and because pirating OEM spares is not straightforward for all technologies (I.e. pumps)

Weir has yet to realize all revenue synergies from the ESCO acquisition (i.e. cross-selling their highly aftermarket intensive ESCO offerings to existing mines); an opportunity which should be highly accretive to margins albeit the smaller size of ESCO.

Lastly, Weir has a long and proven track-record that is relatively straight-forward to assess from the outside (due to consistency in reporting). They have hit most of the crucial milestones over time, and is aligned with shareholders on all fronts.

3. Financial development & valuation

With sales growing at a CAGR of 9.6% (excl. divested segments) from FY18-23A aftermarket sales consistently hovering around 75% of sales, Weir is not as cyclical as some of its project-dependent peers, making it relatively easier to forecast financials with a certain level of conviction. I forecast sales in line with consensus estimates through FY28E, before applying own estimates which are growing at a slightly higher rate (avg. 100bp) than the projected copper demand. Here is the growth projection:

Normally, when forecasting capital goods companies, I’d use backlog turns, book-to-bill, or equivalent (in conjunction with an estimate of “soft” orders) to forecast sales - but given the large portion of sales being labelled as “consumables”, it makes little sense in the case of Weir. In fact, I wonder why they are even reporting order intake (I am not complaining though!).

Margins have trended higher as drag from A&D activities and C-19 have subsided - and management is vocal about its ambition (and progress) toward an adjusted operating profit margin of 20% by FY26. Luckily, the reporting is quite detailed, hence it is relatively straight-forward to reconcile reported and adjusted figures. For my model, I project a slight EBITDA margin improvement toward FY26E as commercial excellence initiatives and ESCO (higher-margin) topline synergies are harvested, before flatlining for the remainder of the forecast period. Note that I adjust for slightly different items compared to Weir’s own adjustments (i.e. my model recognizes share-based compensation as an operating cost, etc.)

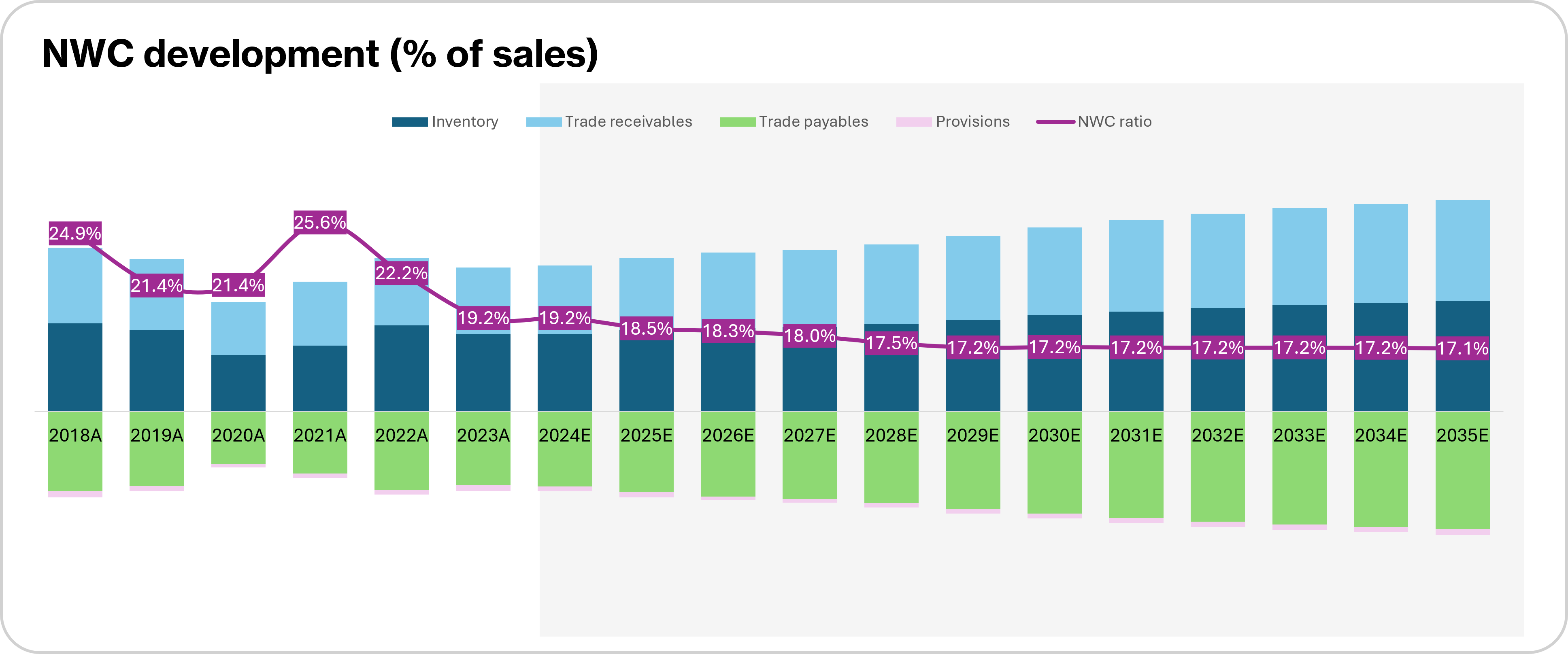

Net working capital has historically hoovered around 21% of sales. I expect management to continue its efforts in securing strong cash generation throughout the forecast period. Admittedly, this is the part of my model where I am less conservative, but for good reason. As industry dynamics change in favor of OEMs, the ability to negotiate terms improves; a similar trend happened during the mining boom of the 2010s.

Given the maturity of the company, CapEx needs are quite limited. This is also evident when comparing CapEx to D&A which tends move within a bands 0.7x - 1.0x. In my estimates, I expect a slight uptick in CapEx (peaking at 1.2x of D&A before tapering to 1.0x when nearing terminal period) to fund growth as competition in the aftermarket domain from FLSmidth and Metso Outotec gets fiercer.

Here is the model output alongside the general assumptions embedded in the DCF. As always, feel free to reach out if anything is unclear and I will do my best to elaborate: